What is the Small Caliber Ammunition Market Overview – definition, scope, and significance?

The Small Caliber Ammunition Market comprises manufactured cartridges of calibers typically ranging from .22 LR up to 14.5 mm, designed for pistols, rifles, and shotguns used by military forces, homeland‑security agencies, and law‑enforcement bodies. The scope includes the complete value chain—from raw‑material procurement (brass, propellant, primer, projectile) through production, testing, distribution, and after‑market services. Its significance lies in the essential role small‑caliber rounds play in modern combat, counter‑terrorism, crowd‑control, and personal‑defense operations, driving sustained demand across both government and civilian sectors worldwide.

What are the key drivers, restraints, challenges, and opportunities influencing the Small Caliber Ammunition Market?

Key drivers include rising defense budgets, modernization programs that prioritize lightweight weapons, and increased procurement by law‑enforcement agencies for non‑lethal and tactical ammunition. The growing popularity of sport shooting and civilian ownership in regions with permissive firearms laws also adds volume. Restraints stem from stringent export controls, environmental regulations on lead‑based projectiles, and fluctuating raw‑material costs. Challenges involve supply‑chain disruptions, especially for critical components like primers, and geopolitical tensions that can limit cross‑border sales. Opportunities arise from the development of polymer‑cased and frangible ammunition, which address environmental concerns, and from the adoption of smart‑round technologies that integrate telemetry for training and battlefield analytics.

Which growth trends are currently shaping the Small Caliber Ammunition Market?

Current trends include a shift toward modular weapon systems that require interchangeable ammunition formats, spurring demand for versatile calibers such as 5.56 mm and 9 mm. There is also a noticeable rise in demand for high‑velocity, low‑recoil rounds that improve accuracy for urban engagements. The market is seeing increased investment in “green” ammunition—lead‑free and polymer‑cased solutions—to comply with emerging environmental standards. Furthermore, digital integration, where ammunition is paired with IoT‑enabled tracking devices, is an emerging trend that offers real‑time inventory management for military logisticians.

How did COVID‑19 impact the Small Caliber Ammunition Market, and what is the recovery trajectory?

The pandemic caused temporary production slowdowns due to workforce restrictions in key manufacturing hubs, leading to short‑term supply gaps. Simultaneously, many governments accelerated defense spending to address security concerns, offsetting the slowdown. Post‑2020, the market rebounded quickly as manufacturers reinstated shift work and adopted stricter health protocols. The recovery trajectory remains positive, supported by pent‑up demand from law‑enforcement agencies and a resurgence in civilian shooting sports as restrictions eased.

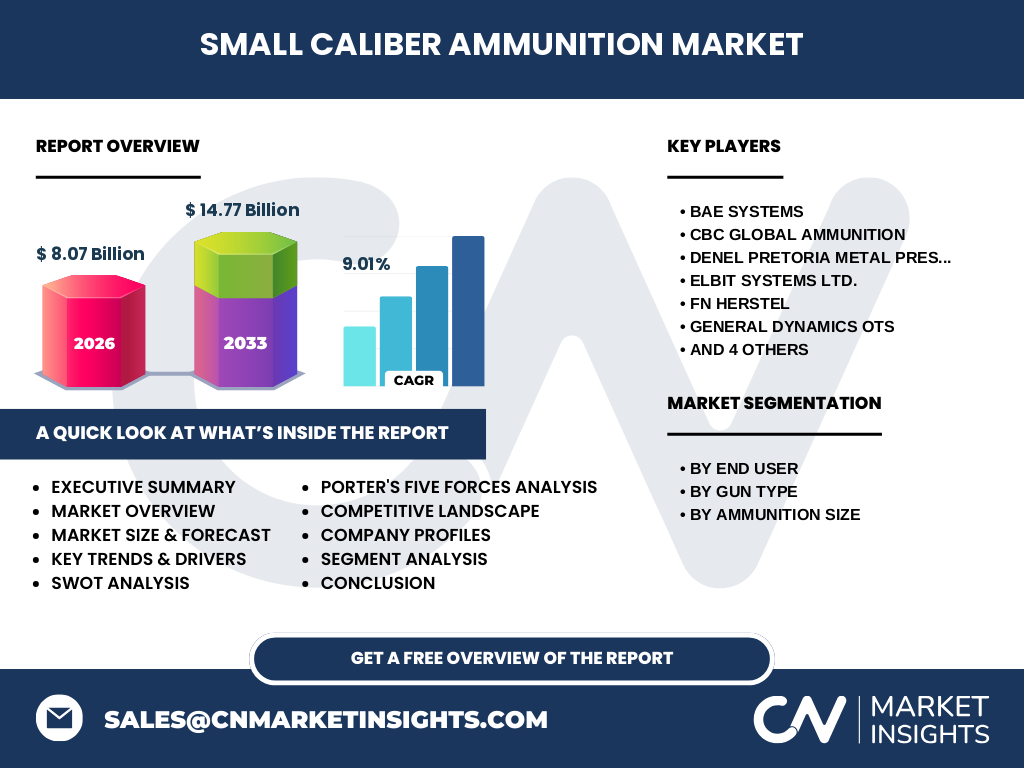

Who are the major competitors in the Small Caliber Ammunition Market, and what is the level of market consolidation?

Key competitors include BAE Systems, CBC Global Ammunition, Denel Pretoria Metal Pressing, Elbit Systems Ltd., FN Herstal, General Dynamics OTS, Nammo AS, Northrop Grumman Corporation, Remington Arms Company LLC, and Winchester Ammunition. The market exhibits moderate consolidation, with a few large multinational firms holding significant share due to extensive R&D capabilities and global distribution networks, while numerous boutique manufacturers serve niche segments such as specialty law‑enforcement rounds.

What are the high‑level findings presented in the Executive Summary?

The Executive Summary highlights a robust market valued at US 8.07 billion in 2026, projected to reach US 14.77 billion by 2033, delivering a CAGR of 9.01 %. Growth is propelled by expanding defense budgets, modernization of small‑arms platforms, and rising demand for environmentally friendly ammunition. While regulatory constraints and raw‑material volatility pose challenges, innovation in polymer‑casing and smart‑round technology offers lucrative pathways for market participants. The competitive landscape is anchored by ten leading firms, each pursuing strategic acquisitions and product diversification to capture emerging opportunities.

What is the forecast for the Small Caliber Ammunition Market from 2025 to 2032?

Based on the provided CAGR of 9.01 %, the market is expected to expand steadily, moving from a 2026 base of US 8.07 billion to approximately US 14.77 billion by 2033. The forecast indicates consistent double‑digit growth throughout the 2025‑2032 horizon, reflecting continued procurement cycles in military and security sectors, as well as expanding civilian market participation in regions with favorable firearms legislation.

How is the Small Caliber Ammunition Market sized and shared across the defined segments?

Segmentation is organized by end‑user, gun type, and ammunition size. End‑users—military, homeland security, and law‑enforcement agencies—collectively account for the bulk of demand, with the military segment typically contributing the largest share due to large‑scale contracts for 5.56 mm, 7.62 mm, and .308 Winchester rounds. Gun‑type segmentation shows pistols (e.g., 9 mm, .45 ACP) dominate civilian sales, while rifles (5.56 mm, 7.62 mm, .223 REM) lead military procurement. Shotgun calibers such as 12.7 mm remain niche but important for specific tactical applications. Ammunition size segmentation reflects a wide product portfolio, with high‑volume calibers (9 mm, 5.56 mm, .22 LR) driving volume, and larger calibers (.338 mm, 14.5 mm) catering to specialized defense needs.

What is the geographic distribution of the Global Small Caliber Ammunition Market?

The market exhibits a worldwide footprint, with North America and Europe retaining the largest shares due to established defense industries and high civilian shooting participation. Asia‑Pacific shows rapid growth, driven by expanding defense modernization programs in countries such as India, South Korea, and Japan. The Middle East and Africa present steady demand, primarily from military contracts and emerging security initiatives.

Can you provide a detailed regional analysis of the Small Caliber Ammunition Market?

In North America, sustained defense spending and a strong culture of sport shooting underpin market stability, with the United States being the largest single‑country consumer. Europe benefits from NATO standardization, driving consistent demand for NATO‑compatible calibers (5.56 mm, 7.62 mm). The Asia‑Pacific region is the fastest‑growing, as governments increase budgets for modern small‑arms platforms and domestic manufacturers scale up production. The Middle East’s market is shaped by procurement for both conventional forces and internal security agencies, while Africa’s growth is linked to peacekeeping missions and capacity‑building programs supported by international partners.

What are the profiles of leading companies in the Small Caliber Ammunition Market and their strategies?

BAE Systems leverages its defense portfolio to integrate ammunition with advanced weapon systems. CBC Global Ammunition focuses on high‑volume production for law‑enforcement contracts. Denel Pretoria Metal Pressing emphasizes cost‑effective manufacturing for emerging markets. Elbit Systems Ltd. invests in smart‑round technologies for precision training. FN Herstal (Herstel) capitalizes on its historic brand to supply premium military calibers. General Dynamics OTS expands through strategic partnerships with NATO allies. Nammo AS drives innovation in lightweight, polymer‑cased ammunition. Northrop Grumman applies its aerospace expertise to develop high‑performance projectiles. Remington Arms and Winchester Ammunition maintain strong civilian market presence through brand loyalty and extensive distribution channels.

How does Porter’s Five Forces framework apply to the Small Caliber Ammunition Market?

Threat of new entrants is moderate; high capital requirements and stringent regulatory barriers limit newcomers. Bargaining power of suppliers is relatively high due to reliance on specialized raw materials (brass, nitrocellulose). Bargaining power of buyers is strong, especially for large government contracts that demand price competitiveness and technical compliance. Threat of substitutes is low, as alternative weapon systems still require small‑caliber ammunition. Industry rivalry is intense, driven by a limited pool of global manufacturers competing on price, technology, and delivery reliability.

What are the SWOT analysis outcomes for the Small Caliber Ammunition Market?

Strengths: Established demand from defense and law‑enforcement; mature manufacturing expertise; high barriers to entry.

Weaknesses: Dependence on volatile raw‑material prices; regulatory complexities across jurisdictions.

Opportunities: Development of eco‑friendly and smart ammunition; expansion into emerging markets with growing security needs.

Threats: Political sanctions affecting trade; rapid shifts in defense priorities that could reduce specific caliber procurement.

What does the value‑chain analysis reveal about the Small Caliber Ammunition Market?

The value chain begins with sourcing of raw materials (copper, brass, lead, propellant chemicals), followed by component fabrication (case forming, primer insertion, projectile molding). Subsequent stages include assembly, ballistic testing, quality assurance, packaging, and distribution to government depots or retail channels. Key value‑adding activities are R&D for performance‑enhancing designs and compliance testing for NATO or ISO standards. Logistics and secure storage constitute critical downstream functions, especially for military customers.

What key investment insights can be drawn for stakeholders interested in the Small Caliber Ammunition Market?

Investors should target companies with diversified product portfolios covering both military and civilian segments, as this reduces exposure to policy‑driven demand swings. Firms leading in polymer‑casing and smart‑round development present higher growth potential given regulatory pressure for lead‑free solutions. Strategic M&A activity—particularly cross‑border acquisitions that expand geographic reach—remains a viable path to scale. Finally, partnerships with defense ministries for co‑development projects can secure long‑term revenue streams.

What conclusions can be drawn from the overall analysis of the Small Caliber Ammunition Market?

The market demonstrates solid, above‑average growth driven by defense modernization, law‑enforcement modernization, and a revitalized civilian shooting sector. While regulatory and supply‑chain challenges persist, innovation in environmentally responsible and digitally enabled ammunition offers compelling growth avenues. The presence of ten dominant players ensures a competitive yet stable landscape, making the market attractive for both strategic investors and technology‑focused entrants.

How was the research for this report conducted?

The research employed a mixed‑method approach, combining secondary data collection from industry reports, government procurement databases, and company press releases with primary insights gathered through expert interviews with defense analysts, ammunition manufacturers, and procurement officials. Quantitative data were cross‑validated for consistency, and qualitative assessments were synthesized to produce the comprehensive analysis presented.

What is the scope of this research, and what limitations should readers be aware of?

The scope covers global market size, segmentation by end‑user, gun type, and ammunition size, as well as regional performance, competitive dynamics, and forward‑looking forecasts to 2033. Limitations include reliance on publicly available financial disclosures, which may not capture proprietary contract values, and the exclusion of classified defense procurement data that could affect precise market‑share calculations.

Which key companies are highlighted, and what recent developments have they announced?

Featured companies include BAE Systems, CBC Global Ammunition, Denel Pretoria Metal Pressing, Elbit Systems Ltd., FN Herstal, General Dynamics OTS, Nammo AS, Northrop Grumman Corporation, Remington Arms Company LLC, and Winchester Ammunition. Recent developments include BAE Systems’ launch of a next‑generation polymer‑cased round, Nammo AS’s partnership with a European defense agency to supply low‑recoil 5.56 mm ammunition, and Elbit Systems’ introduction of a smart‑round prototype featuring embedded telemetry for training applications. Winchester announced a new lead‑free .22 LR line aimed at the civilian market, while Remington expanded its production capacity in the United States to meet rising law‑enforcement demand.